SANTA ANA, Calif., April 2, 2026 —Today, Veros Real Estate Solutions (Veros®),

n industry leader in enterprise risk management and collateral valuation services, released its Q1 2026 VeroFORECASTSM. The forecast projects an average-nationwide home price appreciation rate of 1.3% over the next 12 months.

VeroFORECAST evaluates home prices in over three hundred of the nation’s largest housing markets, and Veros is committed to the data science of predicting home value based on rigorous analysis of the fundamentals and interrelationships of numerous economic, housing, and geographic variables pertaining to home value.

The U.S. housing market finally had a reason to feel optimistic heading into 2026. After years defined by high mortgage rates, limited inventory and stretched affordability, early signals pointed to a shift. Activity was beginning to stir. Buyers were slowly re-entering.

Then geopolitics intervened. The war in Iran sent oil prices sharply higher, reigniting concerns about inflation just as it appeared to be cooling. Financial markets reacted quickly. Treasury yields moved up. Mortgage rates followed. After dipping below 6% in late February, the average 30-year fixed rate mortgage climbed back to roughly 6.4% by late March. That may not sound dramatic, but in today’s market, even small rate movements carry outsized consequences. For many households already stretched by elevated home prices and rising living expenses, a fraction of a percentage point can mean the difference between qualifying for a loan and staying on the sidelines.

And while inflation has moderated from its earlier peaks, it hasn’t fully disappeared. Rising oil prices introduce a new layer of pressure, feeding into transportation, goods, and services costs across the economy. That, in turn, keeps upward pressure on interest rates and limits how far mortgage rates can fall.

At the same time, the labor market is beginning to show weakness. While unemployment remains relatively low in the mid-4% range, job growth has slowed compared to prior years. That shift may seem incremental, but housing decisions are tied closely to confidence in income, job stability, and future financial security. When that confidence softens, so does demand.

Buyers don’t necessarily disappear, but they hesitate. They wait. They run the numbers again. And in many cases, they choose to delay.

On the surface, supply conditions appear to be improving. Inventory has started to rise, giving buyers more options than they’ve had in years. But this isn’t a surge of new listings hitting the market. It’s a slowdown in transactions. Homes are taking longer to sell. Listings are sitting. Meanwhile, many homeowners remain locked in place—literally. There are more homes available than before, but not enough. Mortgage rates are lower than their peak, but not low enough. Demand is still present, but increasingly selective.

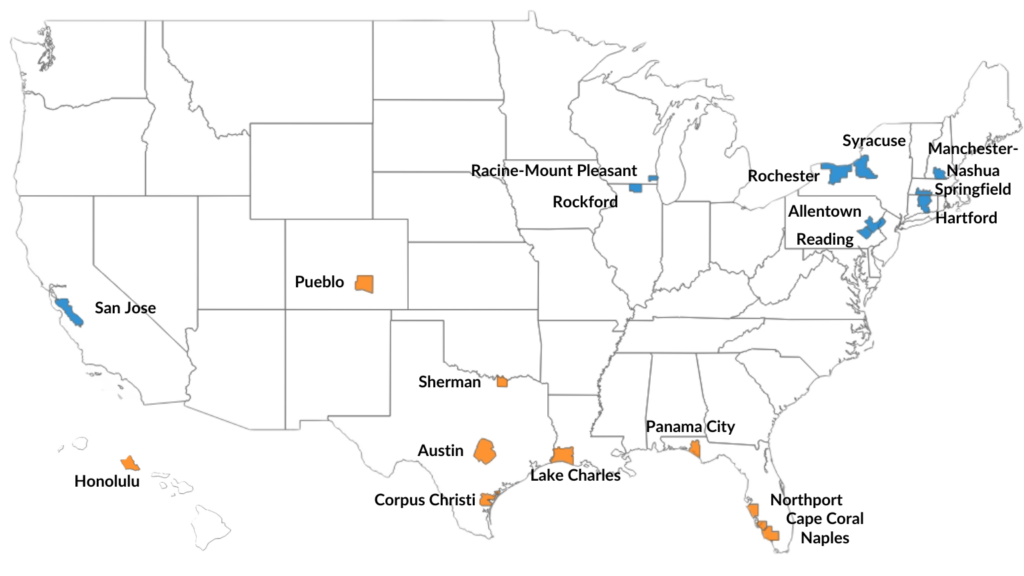

But the national story only tells part of the picture. Beneath the averages, the housing market is becoming increasingly localized. In Northern California, for example, markets like San Jose are seeing renewed strength as capital flows into AI-driven companies, bringing with it a new wave of high-income buyers, many of them with significant cash resources. At the same time, buyers are increasingly drawn to parts of the Northeast and Midwest, where relative affordability and stable economic conditions offer a more accessible path to homeownership.

The strongest-performing markets include Reading, PA; Rochester, NY; Springfield, MA; Allentown-Bethlehem-Easton, PA-NJ; Rockford, IL; Hartford, CT; Racine, WI; Syracuse, NY; and Manchester, NH, alongside San Jose, CA, which stands out due to its exposure to the tech sector.

The 10 Strongest-Performing Markets Over Next 12 Months

| Rank | Markets |

Forecast Data Q1 2026- Q1 2027 |

|---|---|---|

| 1 | READING, PA | 4.2% |

| 2 | SAN JOSE-SUNNYVALE-SANTA CLARA, CA | 4.1% |

| 3 | ROCHESTER, NY | 4.0% |

| 4 | SPRINGFIELD, MA | 4.0% |

| 5 | ALLENTOWN-BETHLEHEM-EASTON, PA-NJ | 3.9% |

| 6 | ROCKFORD, IL | 3.8% |

| 7 | HARTFORD-WEST HARTFORD-EAST HARTFORD, CT | 3.8% |

| 8 | RACINE-MOUNT PLEASANT, WI | 3.7% |

| 9 | SYRACUSE, NY | 3.7% |

| 10 | MANCHESTER-NASHUA, NH | 3.6% |

In contrast, several Sun Belt markets that saw rapid growth during the pandemic are now facing headwinds. Markets such as Cape Coral and Naples in Florida, Austin in Texas, and parts of coastal Florida like North Port and Panama City are among the weakest performers in the latest forecast. These areas have seen a combination of elevated home prices, rising insurance costs, and a surge in new construction, all of which are weighing on demand and increasing competition among sellers.

Other slower-performing markets include Corpus Christi and Sherman-Denison in Texas, Lake Charles in Louisiana, Pueblo in Colorado, and even Urban Honolulu, reflecting how affordability pressures and shifting demand are playing out unevenly across the country.

The 10 Least-performing Markets Over Next 12 Months

| Rank | Metropolitan Statistical Area (MSA |

Forecast Data Q1 2026 - Q1 2027 |

|---|---|---|

| 1 | CAPE CORAL-FORT MYERS, FL | -2.7% |

| 2 | NAPLES-MARCO ISLAND, FL | -1.7% |

| 3 | AUSTIN-ROUND ROCK-SAN MARCOS, TX | -1.4% |

| 4 | PANAMA CITY-PANAMA CITY BEACH, FL | -1.1% |

| 5 | PUEBLO, CO | -1.1% |

| 6 | CORPUS CHRISTI, TX | -1.0% |

| 7 | SHERMAN-DENISON, TX | -1.0% |

| 8 | LAKE CHARLES, LA | -1.0% |

| 9 | URBAN HONOLULU, HI | -0.9% |

| 10 | NORTH PORT-BRADENTON-SARASOTA, FL | -0.8% |

VeroFORECAST Methodology

The quarterly VeroFORECAST reports to clients by subscription and to industry media in a summary overview. The current report is based on 323 Metropolitan Statistical Areas (MSAs) data, including 17,752 ZIP codes, 974 counties, and 82% of U.S. population covered. The report is a projected increase twelve months forward.

Source: Veros Real Estate Solutions

This information is intended for use by the media for economic reporting and should only be used for physical or digital publication or broadcast, in whole or in part, and must be sourced from Veros Real Estate Solutions. The company name must be visible on the screen or website if the data are illustrated with maps, charts, graphs, or other visual elements. For questions, analysis, interpretation of the data, or permission to reproduce, contact communications@veros.com.

About Reena Agrawal, Senior Research Economist

Reena Agrawal has a Ph.D. in Economics from Vanderbilt University. She has fifteen years of experience in macroeconomic forecasting, sectoral research, feasibility studies of complex projects, and preparing reports for multi-national clients.

About Veros Real Estate Solutions

A mortgage technology innovator since 2001, Veros is a proven leader in enterprise risk management and collateral valuation services. The firm combines predictive technology, data analytics, and industry expertise to deliver advanced automated solutions that control risk and increase profits throughout the mortgage industry, from loan origination to servicing and securitization. Veros’ services include automated valuation, fraud and risk detection, portfolio analysis, forecasting, and next-generation collateral risk management platforms. Veros is the primary architect and technology provider of the GSEs’ Uniform Collateral Data Portal® (UCDP®). Veros also works closely with the FHA to support its Electronic Appraisal Delivery (EAD) portal. The company is also making the home-buying process more efficient for our nation’s Veterans through its appraisal management work with the Department of Veterans Affairs. For more information, visit www.veros.com or call 866-458-3767.

Media Contact

Heather Zeller, Vice President of Marketing

communications@veros.com

(714) 415-6300

Original Source via Businesswire