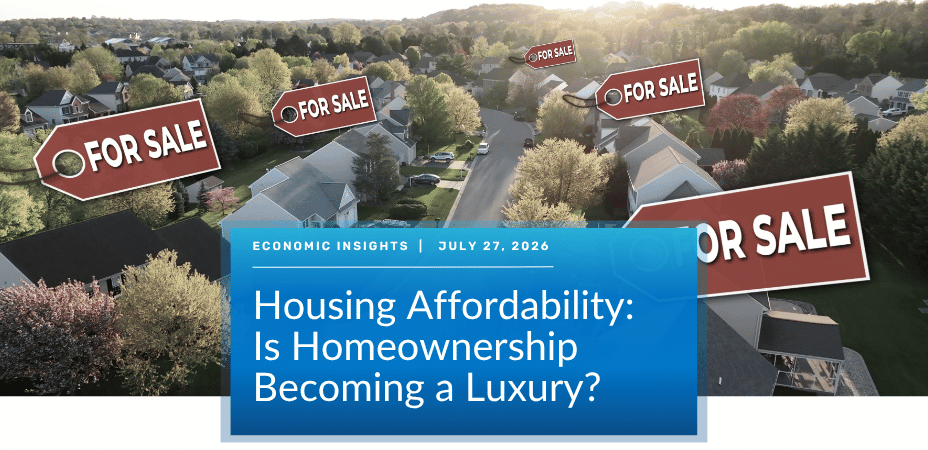

Building Greater Confidence in Your Residential Debt Portfolio

Residential debt portfolios require continuous valuation as insurance costs and market conditions evolve. Discover how private credit fund managers can identify collateral risk, strengthen portfolio management, and improve investor confidence with a more proactive approach.