SANTA ANA, Calif., October 6, 2025 —Today, Veros Real Estate Solutions (Veros®), an industry leader in enterprise risk management and collateral valuation services, released its Q3 2025 VeroFORECASTSM. The forecast projects an average nationwide home price appreciation rate of 1.8% over the next 12 months.

VeroFORECAST evaluates home prices in over three hundred of the nation’s largest housing markets, and Veros is committed to the data science of predicting home value based on rigorous analysis of the fundamentals and interrelationships of numerous economic, housing, and geographic variables pertaining to home value.

The U.S. housing market remains in a holding pattern despite a modest easing in borrowing costs. Mortgage rates have slipped to around 6.3%, and in September 2025 the Federal Reserve delivered a widely expected 25-basis-point rate cut, signaling two additional cuts before year-end. Yet mortgage rates follow the 10-year Treasury yield more closely than Fed policy, meaning a central bank cut does not automatically drive mortgage rates lower. While mortgage rates have retreated from the 7% highs seen earlier this year, the impact on buyer activity has been limited. This is because home affordability remains strained with national home prices roughly 50% higher than at the start of the decade.

The weakening labor market, as new layoffs mount and hiring continues to slow, is also negatively impacting housing demand. The unemployment rate has climbed to its highest level since 2022, and for the first time in four years the number of unemployed workers now exceeds available job openings. Slowing job growth and weakening consumer sentiment have prompted many households to delay major financial decisions such as home purchases. Existing home sales reflect this cautionary behavior, with August existing home sales running at an annualized rate of about 4 million units, which is well below the pre-pandemic pace of more than 5 million.

On the supply side, inventory is improving but still historically tight. The month’s supply of homes rose to 4.6 in August, but this remains low by long-term standards and continues to tilt bargaining power toward sellers in many regions. Many homeowners are choosing to stay put, anchored by ultra-low mortgage rates secured years ago. Instead of negotiating with buyers, a growing number of sellers are simply pulling their listings if they cannot command a premium price. Meanwhile, new construction is struggling to pick up the slack: single-family starts and permits are down roughly 11% year over year, weighed down by elevated materials costs, labor shortages, and tariff-driven increases in imported building products. The result is a market where inventory growth coexists with a persistent shortage of affordable homes, squeezing first-time buyers.

Demographics add another layer of complexity. Baby boomers, born between 1946 and 1964, own a disproportionate share of the nation’s housing stock and increasingly prefer to age in place. Many are investing in home modifications and lifestyle adjustments to remain in their current residences, motivated by emotional attachment and the desire for independence. This choice keeps a large number of well-maintained, family-sized homes off the market, further constraining supply.

However, not all markets are behaving the same, with regional differences driven by economic conditions, supply levels, and local affordability. Metros in the Northeast and parts of the Midwest remain relatively active thanks to limited inventory, comparatively affordable prices, and stable employment in sectors such as government, healthcare, and education. By contrast, several Sunbelt markets are showing pronounced weakness. Here, pandemic-era price surges, rising property taxes, and sharply higher insurance premiums have priced out many buyers, while a growing supply of new construction is creating more competition for sellers.

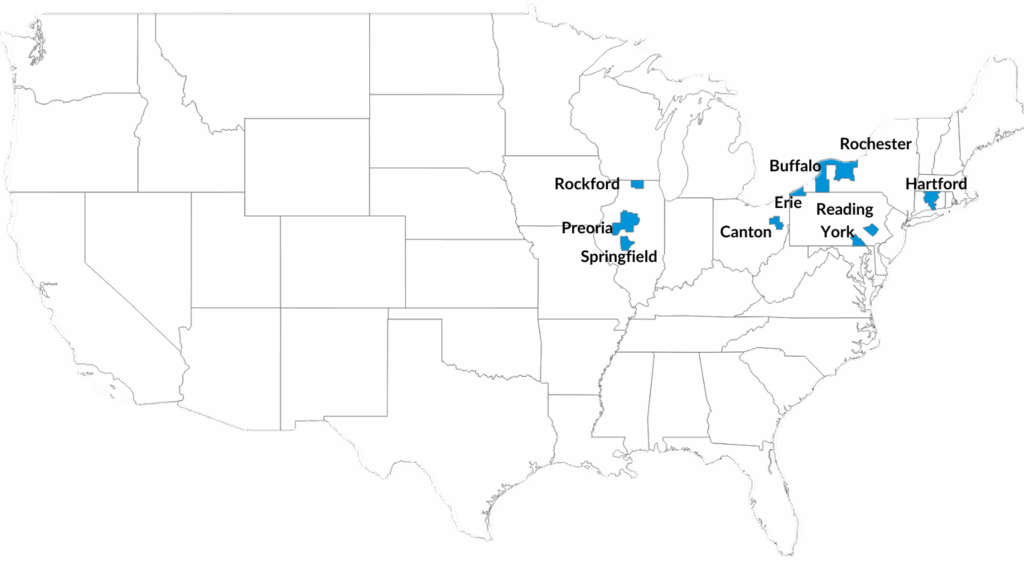

The top ten housing markets projected for the next 12 months include Rochester and Buffalo in New York; Hartford, Connecticut; Rockford, Springfield, and Peoria in Illinois; Reading, York, and Erie in Pennsylvania; and Canton, Ohio. These small and mid-sized metros are outperforming largely because they remain relatively affordable compared to sunbelt markets. Demand is further supported by a slowdown in out-migration from the Northeast and Midwest since the pandemic, which has helped keep buyers active and inventories tight in these regions.

The 10 Strongest-Performing Markets Over Next 12 Months

| Rank | Markets |

Forecast Data Q3 2025- Q3 2026 |

|---|---|---|

| 1 | ROCKFORD, IL | 5.2% |

| 2 | ROCHESTER, NY | 5.1% |

| 3 | BUFFALO-CHEEKTOWAGA, NY | 5.0% |

| 4 | HARTFORD-WEST HARTFORD-EAST HARTFORD, CT | 4.9% |

| 5 | SPRINGFIELD, IL | 4.8% |

| 6 | CANTON-MASSILLON, OH | 4.7% |

| 7 | YORK-HANOVER, PA | 4.5% |

| 8 | PEORIA, IL | 4.4% |

| 9 | READING, PA | 4.3% |

| 10 | ERIE, PA | 4.3% |

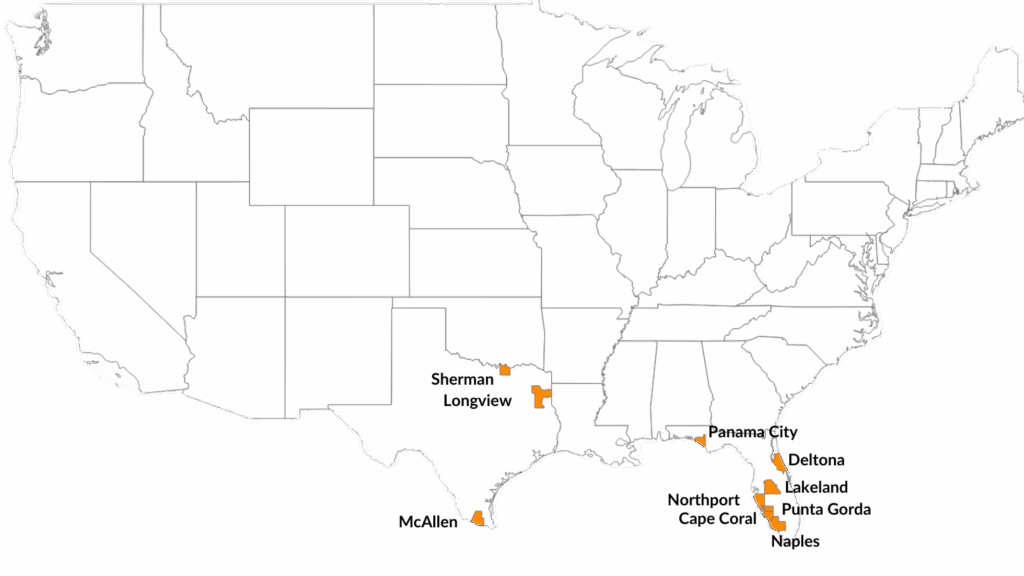

Florida and Texas dominate the list of the nation’s softest housing markets. Both states are grappling with swelling inventories, slowing buyer interest, and persistent affordability hurdles that are weighing on sales. In many metros, new-home construction has surged faster than demand can absorb, leaving properties on the market for longer stretches and prompting price reductions.

The 10 Least-Performing Markets Over Next 12 Months

| Rank | Metropolitan Statistical Area (MSA |

Forecast Data Q3 2025 - Q3 2026 |

|---|---|---|

| 1 | CAPE CORAL-FORT MYERS, FL | -3.1% |

| 2 | NAPLES-MARCO ISLAND, FL | -2.6% |

| 3 | PUNTA GORDA, FL | -2.3% |

| 4 | NORTH PORT-BRADENTON-SARASOTA, FL | -2.1% |

| 5 | SHERMAN-DENISON, TX | -1.8% |

| 6 | DELTONA-DAYTONA BEACH-ORMOND BEACH, FL | -1.6% |

| 7 | MCALLEN-EDINBURG-MISSION, TX | -1.5% |

| 8 | LAKELAND-WINTER HAVEN, FL | -1.5% |

| 9 | PANAMA CITY-PANAMA CITY BEACH, FL | -1.1% |

| 10 | LONGVIEW, TX | -1.1% |

VeroFORECAST Methodology

The quarterly VeroFORECAST reports to clients by subscription and to industry media in a summary overview. The current report is based on 327 Metropolitan Statistical Areas (MSAs) data, including 17,498 ZIP codes, 981 counties, and 82% of U.S. population covered. The report is a projected increase twelve months forward.

- Download the Q3 2025 – Q3 2026 VeroFORECAST results as a PDF infographic

- Download the 10 Strongest-Performing Markets graphic only

Source: Veros Real Estate Solutions

This information is intended for use by the media for economic reporting and should only be used for physical or digital publication or broadcast, in whole or in part, and must be sourced from Veros Real Estate Solutions. The company name must be visible on the screen or website if the data are illustrated with maps, charts, graphs, or other visual elements. For questions, analysis, interpretation of the data, or permission to reproduce, contact communications@veros.com.

About Reena Agrawal, Senior Research Economist

Reena Agrawal has a Ph.D. in Economics from Vanderbilt University. She has fifteen years of experience in macroeconomic forecasting, sectoral research, feasibility studies of complex projects, and preparing reports for multi-national clients.

About Veros Real Estate Solutions

A mortgage technology innovator since 2001, Veros is a proven leader in enterprise risk management and collateral valuation services. The firm combines predictive technology, data analytics, and industry expertise to deliver advanced automated solutions that control risk and increase profits throughout the mortgage industry, from loan origination to servicing and securitization. Veros’ services include automated valuation, fraud and risk detection, portfolio analysis, forecasting, and next-generation collateral risk management platforms. Veros is the primary architect and technology provider of the GSEs’ Uniform Collateral Data Portal® (UCDP®). Veros also works closely with the FHA to support its Electronic Appraisal Delivery (EAD) portal. The company is also making the home-buying process more efficient for our nation’s Veterans through its appraisal management work with the Department of Veterans Affairs. For more information, visit www.veros.com or call 866-458-3767.

Media Contact

Heather Zeller, Vice President of Marketing

communications@veros.com

(714) 415-6300

Original Source via Businesswire