If you’re planning to purchase a home with a mortgage, you’ll need to obtain homeowners’ insurance as a condition of the loan. The American dream of homeownership is facing a new hurdle: rising home insurance costs, coupled with a growing scarcity of coverage in some areas. With record-high home prices already making ownership unaffordable for many, the added expense of insurance is further stretching household budgets. As families struggle to keep up with their monthly mortgage payments, the prospect of soaring insurance premiums adds to their financial worries.

A Nation of Rising Rates

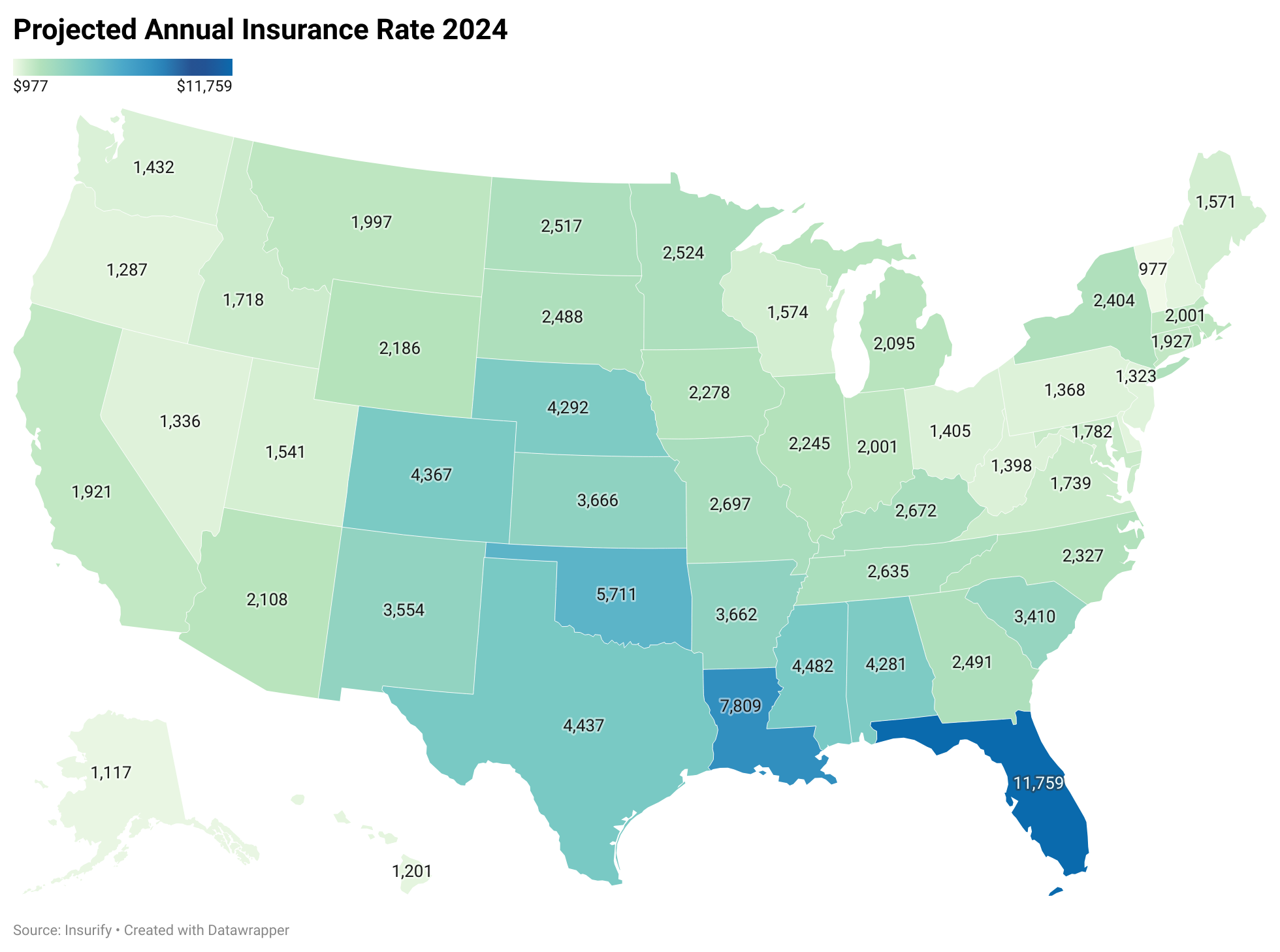

Home insurance costs have been on a steep upward trajectory in recent years. According to Insurify, the average annual rate increased by a substantial 19.8 percent between 2021 and 2023, climbing from $1,984 to $2,377. And the trend shows no signs of abating, with projections for a further 6 percent increase in 2024.

Homeowners in Florida continue to bear the brunt of the highest home insurance rates in the United States, paying an average annual premium of $10,996 in 2023. This burden is expected to worsen, with costs projected to rise by an additional 7 percent in 2024. Louisiana follows closely behind with the second-highest home insurance rates at $6,354 annually. However, Louisiana residents are facing an even more significant increase, with projected costs surging by 23 percent in 2024.

Extreme Weather, Rising Costs

The escalating frequency and severity of extreme natural events, such as hurricanes, floods, and wildfires, are driving up home insurance rates. According to the NOAA National Centers for Environmental Information (NCEI), the United States experienced 28 weather and climate billion-dollar disasters in 2023 alone, resulting in damages exceeding $92.9 billion. Over the past five years (2019-2023), the total cost of billion-dollar disasters in the U.S. has reached a staggering $603.1 billion, with an annual average of $120.6 billion.

It’s crucial to note that these figures represent only a portion of the total cost of weather and climate disasters in the United States, as they only include events with damages exceeding $1 billion. This means they provide a conservative estimate of the annual financial burden imposed by extreme weather. The increasing number and cost of these disasters are attributed to a combination of factors, including increased exposure of assets to risks, vulnerability of infrastructure, and the growing frequency of extreme weather events driven by climate change.

Insurance companies are responding to rising weather-related losses by increasing premiums and, in some cases, limiting coverage in high-risk areas. These changes are particularly challenging for retirees in states like Florida, where home insurance costs are already high. The combined impact of rising premiums and property taxes is forcing many retirees to sell their homes and relocate. Others are returning to work to cover these increased expenses. In regions prone to wildfires, such as California, insurers are discontinuing coverage for homes in certain areas.

Other Factors Influencing Premiums

While there’s a clear link between climate risk and insurance costs, other factors can skew the relationship, leading to premiums that don’t accurately reflect the actual risk. A recent study reveals that insurance rates may not completely reflect associated risks, primarily due to regulatory factors. In states with stricter regulations such as in California, rates often underrepresent actual risks. This discrepancy stems from two primary causes: insufficient rate adjustments for rising losses and cross-subsidization of states with stricter regulations through rate increases in states with lower levels of regulation. Consequently, households in the latter may bear a disproportionate share of risks associated with high regulation states.

For example, consider the case of two neighboring states Wyoming and Montana, with similar weather risks – both states face harsh winters and extreme weather as well as natural disasters like wildfires and floods. The average annual insurance rate in 2023 in Montana was $1,778 compared to $2,159 in Wyoming. But in 2024 rates are expected to increase by 14% in Montana versus just 1% in Wyoming. Policyholders in Wyoming are protected against rate increases by the state government through the Insurance Department, whereas there is no specific protection against rate increases by the state government in Montana. While there are likely other factors influencing the differential rate increases, state regulation could be playing a role. These findings raise concerns about the effectiveness of insurance rates in guiding climate adaptation and the long-term availability of insurance coverage.

The Future of Home Insurance

The entire East Coast is vulnerable to devastating hurricanes, while many Western states face wildfire risks, and Tornado Alley has its own challenges. The increasing cost of home insurance raises concerns about its availability, particularly in regions prone to extreme weather. Climate change, rising construction costs, and reinsurance market changes are all contributing to this trend. As insurance companies face larger payouts and higher costs, they may be forced to increase premiums or reduce coverage, making home insurance less affordable and accessible for many Americans.